When you’re facing financial stress, the idea of filing for bankruptcy can feel overwhelming. At Hoskins, Turco, Lloyd & Lloyd,

Jun 12, 2025

Bankruptcy Posted on Aug 16, 2023

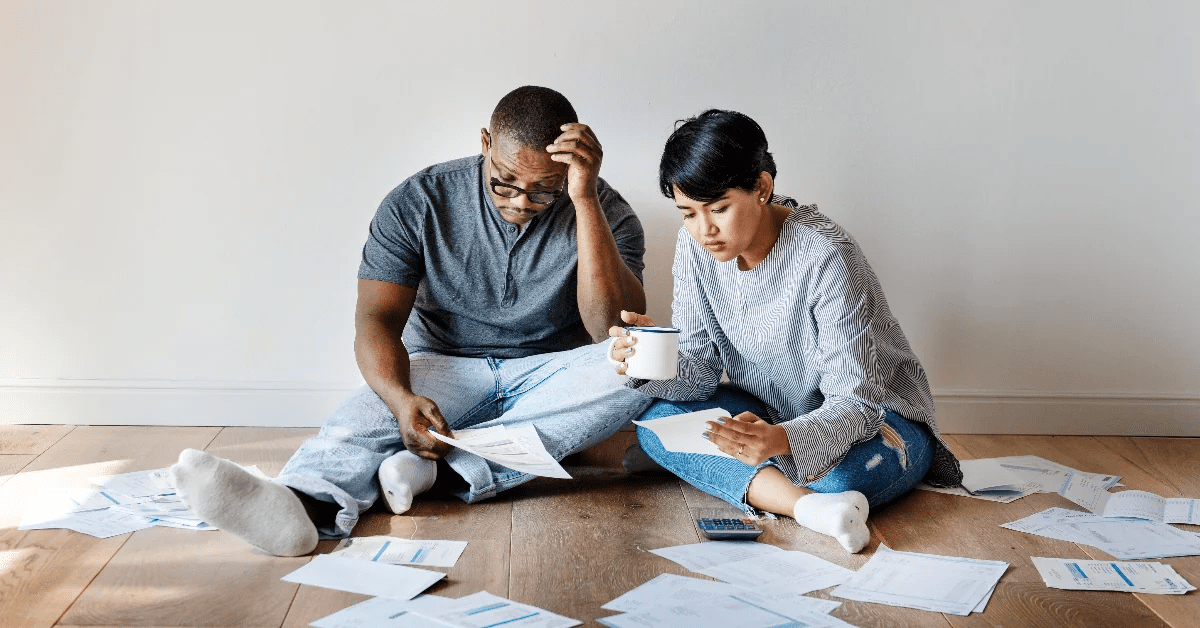

Across the Treasure Coast, families and small businesses are feeling the effects of a tightening economy. In the past twelve months, personal and business bankruptcy filings have increased by 10 percent compared with the previous year. As a result, individuals and businesses within our community are asking our bankruptcy attorneys about the differences between fiing for bankruptcy and debt consolidation. In this blog, we share the pros and cons of filing for bankruptcy or opting for debt consolidation to help you understand your options and and find a debt solution that’s right for you.

Bankruptcy is a legal process that can provide you a fresh financial start by discharing or reorganizing your debts. In Florida, individuals and businesses have several bankruptcy options, with Chapter 7 and Chapter 13 being the most common.

Debt consolidation involves combining multiple debts into a single, more manageable payment through a loan or a debt management plan.

We can help. Call us at 866-930-6435.

If you are a resident or small business owner in Port St. Lucie, Fort Pierce, or Vero Beach, and you are considering filing for bankruptcy or opting for debt consolidation, it’s crucial that you weigh the pros and cons carefully. At Hoskins, Turco, Lloyd & Lloyd, we have a full department dedicated to assisting individuals and business owners with filing for bankruptcy. Our experienced bankruptcy attorneys have helped hundreds of St. Lucie County and Indian River County residents and businesses get a fresh financial start.

We will help you navigate the complexities of bankruptcy law, provide personalized advice, protect your rights, streamline the process, and maximize the benefits available to you. Our expertise and support will make a significant difference in your bankruptcy experience and ensure the best possible outcome for your financial future.

We offer free bankruptcy consultations to help you understand your legal and financial options. Call us today at 866-930-6435 to schedule your complimentary meeting.

When you’re facing financial stress, the idea of filing for bankruptcy can feel overwhelming. At Hoskins, Turco, Lloyd & Lloyd,

While the holidays can bring joy, they can also lead to financial stress if not managed carefully. Here are 7

Filing for bankruptcy is a significant decision that can have long-lasting effects on your financial health and personal life. It’s

Phone: (772) 344-7770

Fax: (772) 344-3838

Phone: (772) 464-4600

Fax: (772) 465-4747

Phone: (772) 577-7551

Fax: (772) 794-7773

Phone: (863) 357-5800

Fax: (863) 763-2237

As the law firm Florida has trusted for over 40 years to fight on their behalf, we are more than ready to represent you. Put our experience and reputation to work. If you need help with any legal matter, whether it’s a personal injury, workers’ compensation, disability or bankruptcy case, contact us now. The consultation is absolutely free.

Get the answers you need. We’ll review your case today, for free.

"*" indicates required fields

Port St. Lucie

Port St. Lucie